The ins and outs of surrogacy insurance

The $30,000 Question to Ask Before Transfer

Of every confusing topic in the surrogacy journey, insurance was the hardest for me. Later I found out that it is also one of the biggest cost variables. Depending on the surrogate’s existing coverage, state, ACA timing, and lien risk, insurance can move your total journey cost by $20,000–$30,000, sometimes more.

That is why I wrote this post: to give other intended parents (IPs) a basic map, so you can actively avoid the pitfalls before the match is already emotionally locked in.

This article is based on an ART Risk webinar, an interview with ART Risk CEO Sarah Paige, and our own experience working with our agency and lawyer. I’m not an insurance broker. Treat this as a starting framework, not a replacement for actual policy validation.

TL;DR

Surrogacy insurance is necessary to cap your financial exposure if complications happen during pregnancy or delivery. There are 3 paths for medical insurance:

- The dream scenario is that your surrogate has surrogacy-friendly insurance;

- The most common path is to enroll the surrogate onto an ACA/Marketplace plan;

- In edge cases, commercial policies tailored for the surrogacy market are available, but that is not the focus of this article.

- If your surrogate already has surrogacy-friendly insurance, it can be one of the biggest money savers in the journey. But not many surrogates have this, so making it a hard selection criterion may shrink your pool significantly.

- If her current insurance is not usable, an ACA/Marketplace plan is often the best fallback, but timing matters. You generally need to wait till the Open Enrollment period in Nov-Dec.

- In some states and with some insurance carriers, ACA plans may create lien risk. If your surrogate is in one of those states, treat the lien as a budget line item, not a surprise.

- Regardless of which plan covers the pregnancy, IPs should expect to pay the surrogate’s pregnancy-related co-pays, deductibles, and out-of-pocket maximums.

- Get the insurance review early. Some of your best options may disappear once your surrogate is pregnant.

- Do not forget life insurance and loss-of-reproductive-organs / serious complication coverage. These are separate from medical insurance and usually handled through the Gestational Carrier Contract (GCA).

Why Insurance vs Paying-Cash?

The price for medical insurance is actually comparable to a uncomplicated pregnancy. But insurance isn't really for the best-case pregnancy. It is for the complication scenario, the version where the medical bills get expensive very quickly.

One example from the ART Risk webinar: a surrogate had what looked like a normal delivery. No NICU. No C-section. Out of the hospital in 2.5 days. But she needed 3 blood transfusions afterward, and the final bill was over $60,000. With major complications, the number can easily move into the six figures.

The real question isn't "can we afford the best-case pregnancy?" It's "can we afford the worst-case one?"

For most IPs, the answer to that second question is no. That's the core reason for insurance.

The cash-vs-insurance question isn't really a choice if your surrogate is in New York State (NYS): the Surrogates' Bill of Rights in NYS requires the surrogate to have a health insurance policy, paid for by the intended parents, covering the full pregnancy from before embryo transfer until 12 months after .

The three paths of surrogacy insurance

The framework that helped me most is to understand the 3 paths of surrogacy insurance. This came from the ART Risk webinar, and once I had it, the whole topic clicked.

Path 1: The surrogate’s existing insurance is surrogacy-friendly

This is the dream scenario.This can be one of the biggest money savers in the journey - sometimes in the $20,000–$40,000 range.

The surrogate keeps her existing plan, IPs pay or reimburse the relevant premiums depending on the contract, and her insurance covers the pregnancy like any other pregnancy.

In practice, I have not seen many surrogates with surrogacy-friendly plans, so making it a hard selection criterion may shrink your pool significantly.

Note that IPs are still responsible for pregnancy-related co-pays, deductibles, and out-of-pocket maximums. But the cost is dramatically lower than buying a new policy.

Path 2: The surrogate doesn't have surrogacy-friendly insurance.

This is the most common scenario: the surrogate's existing insurance has a surrogacy exclusion, or she has no usable coverage. In this case, ACA is a great fall back, with two most common structures:

- ACA / Marketplace plan as primary coverage. This is often the most cost-effective fallback, assuming timing works and the plan is usable in her state.

- Short-term medical plan plus ACA later. This can be used as a bridge when the transfer timeline does not align with Open Enrollment.

There are other variations (her existing plan as primary with an IP-paid secondary, etc.), but overall, ACA is the workhorse here.

Path 3: Maternity-only or specialty policies

If ACA somehow is not available to certain surrogate, there are commercial policies sold specifically for the surrogacy market. The premiums can be high, and it is the fallback when the cleaner routes do not work. I did not go deep into this route because it was not the primary path for our match.

ACA is great, but read the fine print on these two things!

ACA / Marketplace coverage can be a great option, but has two major caveats: enrollment timing and lien risk.

1. You can only enroll during open enrollment

ACA open enrollment runs roughly 11/02 through 01/15 in most states. In practice, this means your match timing matters. If you match in February and transfer in March, and your surrogate doesn't have surrogacy-friendly coverage, you may need to bridge the gap with a short-term policy until the next open enrollment in November, and then enroll her in ACA for the actual delivery year.

In our case, we matched in May. If everything goes well, the transfer would be around August. The working plan looks roughly like this:

- Aug – OctUnder the IVF clinic

The surrogate is in the clinic's care for the first ~10 weeks after transfer.

- Oct – DecBridge the gap

Negotiate cash-pay rates for her OB care, and buy a short-term plan ($2K–$3K) to cover complications — with an effective date before pregnancy.

- Nov – DecEnroll in ACA

Open enrollment. Sign her up for the Marketplace plan that will cover the delivery year.

- Jan 2027 →Delivery year

ACA coverage carries the pregnancy the rest of the way through birth.

Note that the option to purchase short-term insurance disappears once the surrogate is pregnant. This is exactly why the insurance review cannot wait until pregnancy. The plan must be locked in before the calendar and clinical timelines eliminate your options.

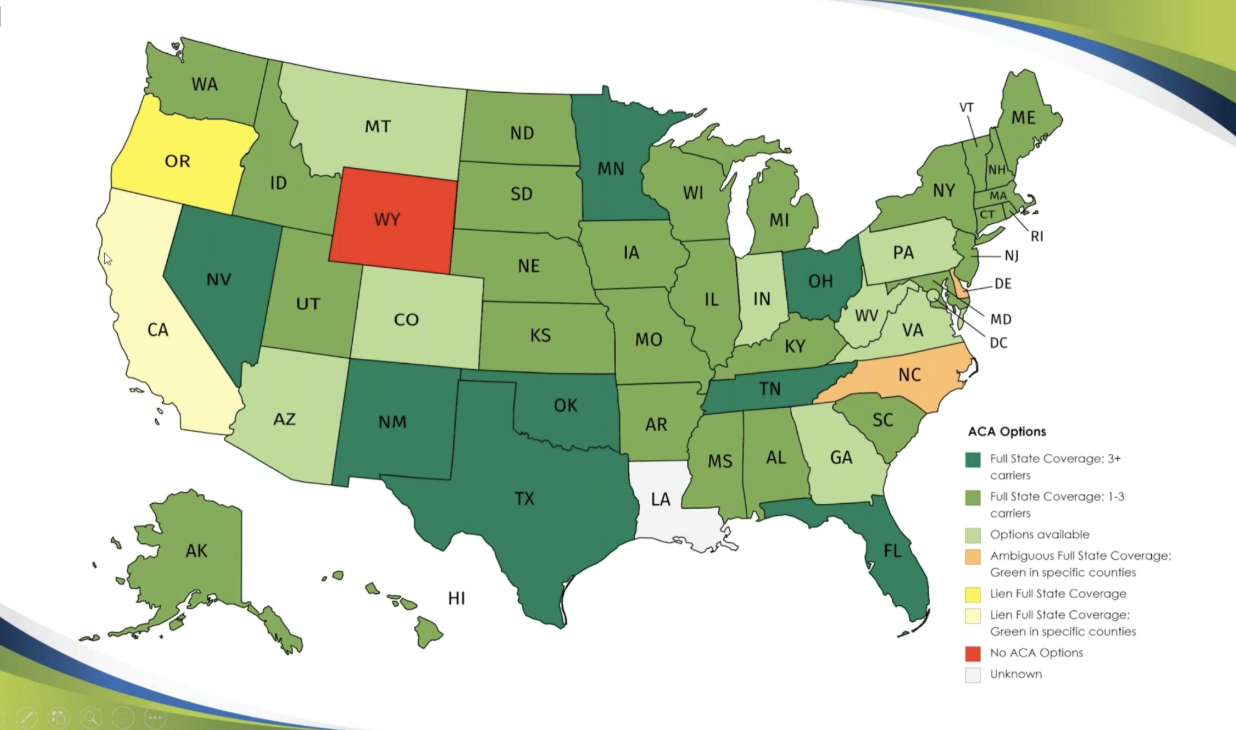

2. In some states, ACA carriers place liens, and IPs pay for it.

This is the part that catches many IPs off guard. A lien is the insurance carrier's claim to recover some of the medical costs it paid, on the argument that the pregnancy was "commercial" or "non-personal".

In a 2024 interview, Paige, the CEO of ART Risk, estimated her firm sees 400 - 500 surrogacy arrangements per year directly impacted by liens, and over 600 surrogates per year switching insurance specifically to escape lien language. They depend on the state, the carrier, and sometimes even the specific plan or ZIP code. The amounts can also vary significantly. Some may be capped at a percentage of the surrogate’s base compensation; others may be tied to the actual medical claims paid.

A few practical points:

- Lien-free coverage depends on the state and carrier. The map below shows the 2021 landscape, but this changes over time. In the December 2025 interview, Paige, said something that surprised me: when asked whether she would still recommend a California surrogate today, she said she probably would not, mainly because of insurance. That went against my prior assumption that California was one of the most surrogacy-friendly states.

- Liens are carrier-specific, not universal. Per my attorney, In California, Anthem does not impose liens, while Kaiser and Blue Shield of California do. Other states have their own patterns.

- “Liens are always negotiable!” …per my attorney. A real example from that attorney: a Kaiser lien claim came in at $25,000 and was settled for $6,000.

- The way you verify lien exposure is a "policy validation": typically around $400–$500 through vendors like ART Risk and should be done before signing a contract with any surrogate whose insurance will be used.

If your surrogate lives in a state where lien exposure is real, plan for the lien as a line item in your budget, not as a vague tail risk. A budgeted $10,000–$25,000 lien exposure that you negotiate down is a far better outcome than a $25,000 surprise that arrives during delivery month.

The cost most IPs forget - co-pays, deductibles, out-of-pocket max

Even with a good insurance setup, IPs are typically responsible for the all the medical cost through out the surrogacy journey, including:

- Prenatal appointment co-pay.

- The full deductible on her plan ( $1,500–$8,000 depending on policy).

- The out-of-pocket maximum if the pregnancy is high-risk or involves a C-section (often $7,000–$15,000 in-network).

- out-of-network charges for monitoring clinics, specialists, labs, anesthesia, or hospital services.

I would build a placeholder of $10,000–$15,000 into the budget for this category. it is not always obvious in agency cost sheets, but it is very likely to happen.

Life and Complication coverage

Most surrogacy contracts require IPs to provide some combination of:

- Life insurance for the surrogate, often in the $250,000-$750,000 range (New York requires a $750,000 minimum, see below), payable to her family if she dies during or as a result of the pregnancy. This can be covered through a term life policy.

- Loss-of-reproductive-organs or serious complication compensation, often in the $50,000–$100,000 range, payable to the surrogate if she loses her uterus, ovaries, or fertility as a result of the journey. This can be covered through a rider policy on top of the life term policy, or compensate the surrogate directly in cash if those events occur.

The Surrogates' Bill of Rights in NYS mandates the life policy must carry a minimum benefit of $750,000 (or the most the surrogate can qualify for, only if she can't qualify for the full $750k).

These policies are inexpensive relative to the rest of the journey, but they should be handled before embryo transfer, not in the final week.

The questions I wish I'd asked

If I were evaluating a surrogate profile today, I would not stop at "insurance looks good." I would ask the following questions. You do not need to answer all of this yourself. That is what attorneys and agencies are for. But you do need to know enough to ask.

- What insurance does she currently have? Is it employer-based, spouse-based, ACA / Marketplace, Medicaid, military, or something else?

- Has the actual policy been formally reviewed for surrogacy?

- Does it exclude surrogacy, assisted reproduction, or compensated pregnancy?

- Does it include lien, reimbursement, subrogation, or third-party recovery language?

- What are the deductible, co-insurance, and out-of-pocket maximum?

- Are her OB, hospital, MFM if needed, and labs in network?

- If the policy renews during pregnancy, could terms change?

- If her job or spouse’s job changes, what happens?

- If the current insurance is not usable, can she enroll in ACA during the needed window?

- If ACA is the plan, what is the open enrollment timing in her state?

- What life insurance is required by contract?

- Are there organ loss or serious complication compensation terms?

You don't have to become the insurance expert. You just have to refuse to be the person who never asked.

Get the review early, treat liens as a line item, and put the life and complication coverage in place before transfer. The worst-case pregnancy is exactly what you're insuring against — make sure the coverage is real before you need it.